“It’s just 2k for the shoes. I can save next month!”

“I feel like having some Big Square chicken wings today. I should be able to spoil myself sometimes!”

“2020 was tough! To better things in 2021! #SelfLove”

Which of these lines sounds like you? Ama niwache kimbelembele? Lol! How often do you have this conversation in your head before an obviously poor financial decision you often regret 90% of the time? Unless in cases of witchcraft (0.001% of the time), our daily financial decisions are choices we make. It is therefore up to you to decide if these decisions you’re making are conscious or unconscious? Helpful or detrimental? Constructive or destructive?

Today, I’d like to point out 5 mistakes that we often make which if taken in isolation, are usually harmless but over a period of time, make a significant dent in our overall financial wellness.

1. Keeping up with the Joneses

FOMO is a trap! How many times have you seen the “latest” of literally anything? The latest phone, car, watch, fashion trend…It’s a wonder to think that it’s actually possible to keep up and an even bigger wonder that someone actually tries to keep up. It’s a rat race that has no end and your finite coins can’t possibly cope with the infinite ideas coming up literally every day! The reason, I believe, this whole ‘What’s trending’ mentality works is because of the allure and temptation of constant comparison coupled with the desire to fit in.

“She has the new Dior scarf so it must be cool. I need to have it too.” A version of this statement goes through our minds consciously or unconsciously every time we fell the need to get something which adds absolutely no real value to our lives. I say ‘real’ value because three more superficial friends who think you’re cool because of the scarf and a few more likes on social media isn’t real value.

For us mums, we sometimes compare everything down to the head band that Rita’s kid is wearing which is super cute on her kid and we think of how cute it would look on ours. It just might be but what’s really your reason for the purchase? The trends will never end. That’s why they’re trends; they’re fleeting. Find what works for you within your own budget and ability to keep up (Lord knows some of us don’t have the energy), and stick to it. The constant desire and attempt to live up to unrealistic personal and societal expectations of yourself will absolutely destroy your finances.

Ask yourself: What am I putting my energy towards that’s costing me financially but reaping not real benefits?

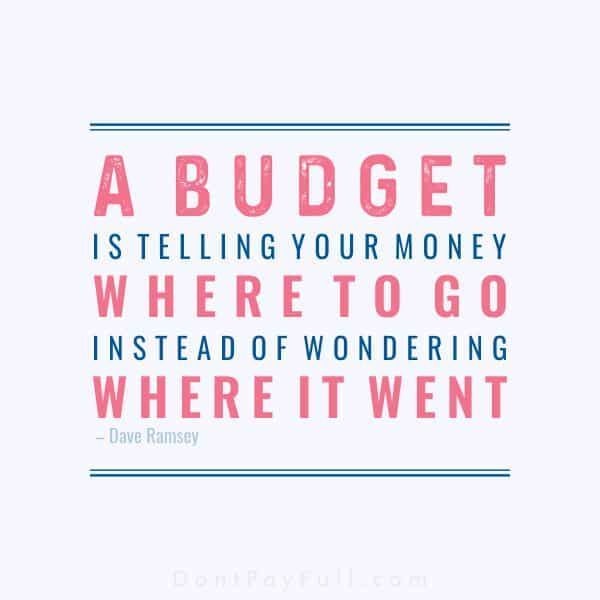

2. Failure to plan your spending

Anything worth doing and sustaining needs a plan, and that includes your money. Planning your spending is also called budgeting. I know people don’t quite like this idea because it sounds very restrictive but I assure you that it’s actually quite liberating. When you have no plan then what’s not at the mercy of your landlord, KPLC and GoK is at the mercy of your whims; basically a situation of ‘pick a master.’ However, with a financial plan, you decide where that money goes thereby giving you control. Think about it, how many have you said or thought “Where has all my money gone this month??” Yet you probably don’t earn any more than you did last month and if things stay as they are, you’ll earn the same next month.

The only solution is to be more intentional with your spending by doing just two things: First, track your spending to know what you spend on. I once heard that you often spend more on food than you think you do. I didn’t think it was exactly true until I started tracking my own spending then realized they weren’t at all wrong. Identify all your streams of expenditure of money from your pocket and assign each of them a value that you can stick to. If you’ve assigned Ksh. 10,000 to eating out that month, give it Ksh. 2500 a week then work within that budget. When you have a set limit, you’re conscious of how you spend within that limit. You just might realize that since you have a high school reunion next week and you may spend Ksh. 3,000, then you can pass up that KFC today which you know you don’t really need.

Ask yourself: What do I actually spend my money on and how can I make that spending more efficient by making a proper financial plan?

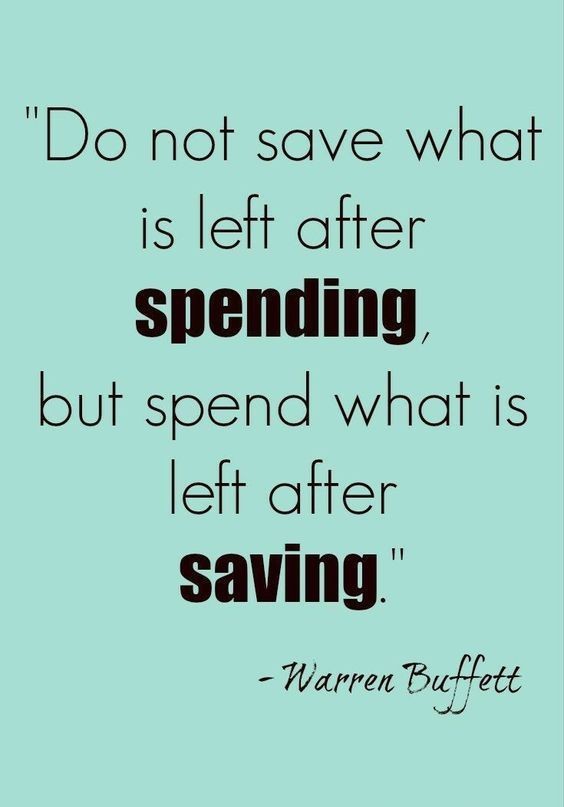

3. Spend then save what’s left

If there is a mistake that destroys our finances more than anything, then this is it, and it flows off the last mistake about not planning your spending. “Kesho pia ni siku” (Translation: Tomorrow is another day) has been one of the most misused statements just before a horrible financial mistake. There’s a Chinese common saying which goes “The best time to plant a tree was 20 years ago. The second best time is now.” Similarly, the best time to have started saving and investing in your money tree would have been several years ago. The second best time would be now. And the only way to be successful at saving and investing is making it a discipline which is developed through deliberate and consistent efforts; you can’t ‘wing it’ at financial success. As you make a plan for all your expenditure streams, direct at least one stream towards saving and investing (in my last post, I explained that the two are not the same).

It is recommended by various financial advisors that you should ideally save up at least 10% of your income. However, even diligence in 5% of it will take you a long way as long as it is developed into a habit rather than a ‘depending on the situation’ kinda thing. What happens is that we often spend then hope to save what’s left but that’s putting the cart before the horse because hope isn’t a strategy. Save then spend what’s left.

The fear is that you may not have enough to take you through the month if you do that but like my brother says “You can’t spend what you don’t have.” How many times have you seen something you absolutely love and want to have then ask about the price and figure you’re given suddenly diminishes 50% of the appeal of that item? You tell yourself “Hata si kali vile nilidhani” (Translation: It’s not even as cute as I thought). You realize that you can go through life just fine without that coat you saw hanging outside that shop; you already have three in the closet you don’t use anyway!

Ask yourself: What am I spending on today that is robbing me of a great financial future?

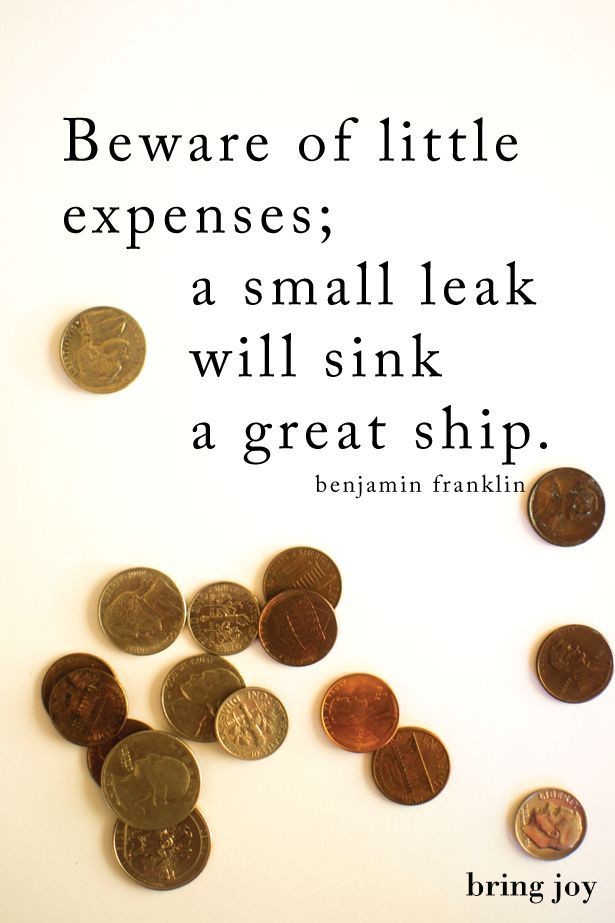

4. Convenience over cost

I’ll give my example for this one. I usually need to get around from my house to wherever I’m going and I often walk, get a motorbike, matatu or cab depending on various factors like time, distance, whether I’m alone or with my daughter etc though often, it’s just me. The most efficient is a motorbike. It’s faster than the others and gets me to almost exactly where I need to go which makes it most convenient. When headed to town, it will cost me between Ksh.50 and Ksh.100 (depending on the destination) on a motorbike or Ksh.30 in a matatu. While it may be faster to take a motorbike, it’s more expensive. Now, you may say that the difference in cost is about Ksh. 30 which is quite little. However, that Ksh.30 in one day translates into Ksh. 150 a week and Ksh.600 a month, on the lower side for a one way trip and for the minimum distance I usually have to go.

Calculate what that would mean on days when I have errands in different parts of town and/or have to go to town more than once in a day. When I became aware of that difference, I began to find ways to limit unnecessary expenditure. For example, rather than take a motorbike to the market which would cost me Ksh. 70, I take a matatu to the stage which costs Ksh.20, walk the rest of the way to the market and take a motorbike back because I often have heavy luggage when I leave the market. I also walk to or from work and save the Ksh.50 as well.

It may need you to leave the house early to take the walk, or take the matatu and walk the rest of the way. You may not need that cab ride to leave the coffee date but you might need it when leaving the supermarket after doing the month’s shopping. You might not need that take-out food just because it’s payday but you might need it after that long journey and you don’t have the energy to cook. When we limit the cost of unnecessary conveniences, we have more to spare when we really do need the extra money.

Ask yourself: What conveniences can you forego to save a few extra, and often unnecessary, costs?

5. YOLO

Your interpretation of that word is often an accurate depiction of your financial status. Society, youth in particular, have coined this phrase to mean that you have to live your best life today because tomorrow isn’t promised. While this may be absolutely true, it is also a reality that tomorrow may not be promised but it is a possibility. The question then becomes: How well are you preparing for it? My pastor used to phrase this very comically but it makes absolute sense. He would say “Wengine wenu mmekula simiti ya foundation ya nyumba yenu!” (Translation: Some of you have already ‘eaten’ the cement for the foundation of your house.) One bag of cement is about Ksh. 800 which may also be the cost of one plate of food at Java. If you decide to cook at home with the groceries you bought at the market the day before, you’ll have spent way less, if at all, and managed to put some money aside for other needs you may have.

Apart from simply saving money by not spending, another mistake is that the money is not saved in a place where it can grow. Because YOLO, you want the money you put aside to grow and meet your future needs or at least manage to keep up with the rising cost of living. How? By investing it in a place where it can multiply. Waithaka Gatumia gave an example of how if you save Ksh. 300 per day for 20 years in a place which gives a return of 10% per year, you will have over Ksh. 6million at the end of that period simply by harnessing the power of compound interest. While it may seem like a big dream, the key is always consistency and patience. Nothing worthwhile happens overnight; you have to master the almost forgotten art of delayed gratification. This is especially possible when you’re single and have no kids yet because kids are amazing but there’s a cost to raising them. Prepare for them now to make it easier when they come along.

Ask yourself: What can you forgo today and invest to secure your financial future tomorrow?

Even if you’re guilty of any or all of these mistakes, even now is a great time to start that journey towards financial success. Even if you save as little as Ksh. 500 every month, it’s better than having nothing at all. Track your spending, stop comparing yourself to others, save before you spend, limit unnecessary costs for convenience and master the art of delayed gratification. These small and simple but conscious efforts will develop into cornerstones of your financial journey. See you at the top!

Thanks for sharing Stacy

Thanks for reading Mercy 😊

Wow,so insightful!

Thanks 😊

**back biome**

Mitolyn is a carefully developed, plant-based formula created to help support metabolic efficiency and encourage healthy, lasting weight management.

Your point of view caught my eye and was very interesting. Thanks. I have a question for you.